“ LVMH Bets on Booze-Free Bubbles at $100-Plus a Bottle” was the Wall Street Journal headline. The story, which you may have read when it came out last month, is that luxury goods conglomerate LVMH was buying a 30 percent stake in a (luxury) non-alcoholic wine start-up called French Bloom. The new NA wine boasts both good DNA (one of the founders and the winemaker are members of the Taittinger Champagne clan) and a bold business plan. The WSJ reports that

LVMH Bets on Booze-Free Bubbles at $100-Plus a Bottle” was the Wall Street Journal headline. The story, which you may have read when it came out last month, is that luxury goods conglomerate LVMH was buying a 30 percent stake in a (luxury) non-alcoholic wine start-up called French Bloom. The new NA wine boasts both good DNA (one of the founders and the winemaker are members of the Taittinger Champagne clan) and a bold business plan. The WSJ reports that

The brand sells bottles of sparkling white for $39 and sparkling rosé for $44, mostly in high-end bars and restaurants, or through luxury retailers. Its latest nonalcoholic fizz, La Cuvée Vintage 2022, which accounts for a small percentage of its production, sets consumers back $119 a bottle.

While the brand initially expected customers would mostly be pregnant women and nondrinkers, it estimates that about 80% of its clients drink alcohol.

NA Wine Challenges and Opportunities

I think the logic of the investment was pretty simple for LVMH. Someone is going to develop a non-alcoholic luxury sparkling wine brand, so they might as well do it themselves and capture the high end of the market. The acquisition is driven, at least in part, by the same logic that led Moet Hennessy to create an international network of wineries to satisfy the local thirst for sparkling wine. Argentina, California, Australia, China, and India. And now in NA-land, too.

What I found particularly interesting about the French Bloom article was the discussion of winemaking challenges. Making quality NA wine or beer is not as easy as just taking the alcohol out. Millions of dollars are being invested in innovative processes to make the NA products as appealing as their alcoholic shelf-mates. The WSJ reports that,

When a wine is dealcoholized, it loses about 60% of the aromas. “We have to start with something that has, we like to say, wider shoulders, versus if you dealcoholized a Chardonnay from Burgundy, you’re not left with a lot,” …

French Bloom sources its grapes from the Languedoc region of southern France, where the sunny climate results in grapes with naturally high alcohol content and sugar levels. They also harvest the grapes two to three weeks early, depending on the year, to have maximum acidity. They then age the wines in new oak barrels from Burgundy. … The wine is “undrinkable before the dealcoholization process,” said Frerejean-Taittinger. “It’s so overpowering.”

The goal, as we here at The Wine Economist have proposed, is for NA wine to pass the “Second Glass Test.” An NA wine should remind us of the type of wine it represents (an NA Sauvignon Blanc should remind us of a Sauvignon Blanc) and it should be good enough that you ask for a second glass. It is a simple test but, as we reported last year, one that many wines seem to fail. Either they don’t really taste like the wines they mimic or they just aren’t that fun to drink. Sad!

Bolle Sparkling Wine Passes the Test

LVMH’s investment in French Bloom provides evidence, if any is needed, that NA wine is a thing. We haven’t had an opportunity to put French Bloom to the Second Glass Test yet, but we could not resist an invitation from the makers of Bolle Non-Alcoholic Sparkling Wines to give their wines a test drive.

LVMH’s investment in French Bloom provides evidence, if any is needed, that NA wine is a thing. We haven’t had an opportunity to put French Bloom to the Second Glass Test yet, but we could not resist an invitation from the makers of Bolle Non-Alcoholic Sparkling Wines to give their wines a test drive.

I was intrigued by the innovative production process. There are several ways to remove alcohol (French Bloom uses a process called vacuum distillation). The Bolle method first ferments the grape juice in the usual way, removes the alcohol, then adds a little grape juice, and allows a second fermentation to replace some of the characteristics that were lost earlier in the previous process. It is a clever idea, don’t you think?

The resulting wine has less than 0.5 percent ABV, which is within the “non-alcoholic” range. Does the second fermentation put the magic back in the bottle? Does Bolle pass the Second Glass test? There was only one way to find out.

We tried the Bolle sparkling Rosé and were quickly convinced: this is probably the best NA wine we have tasted so far. Did it remind us of Blanc de Noir sparkling wine? Yes. Would we accept a second glass? Absolutely. The wine was nicely balanced, dry, but with some of the fruit that we have found missing in earlier “second glass” trials. Whatever they are doing at Bolle the results are excellent.

The Bolle sparkling Rosé is made with a combination of Chardonnay and Pinot Noir wines. We are looking forward to trying the Bolle sparkling Blanc de Blanc, which is Chardonnay blended with Sylvaner. The grapes are from Spain and the NA wine process happens in Germany. Production is still quite limited, so the best way to purchase Bolle is probably directly from the winery website.

Abstinence NA Spirits

As long as Sue and I were testing NA wines we could not resist an invitation to expand our experiments to include a NA spritz product. One of the best things about a trip to Italy is the excuse it provides to enjoy an Aperol or Campari spritz. We make them at home, too, and they bring back that warm Italian feeling.

As long as Sue and I were testing NA wines we could not resist an invitation to expand our experiments to include a NA spritz product. One of the best things about a trip to Italy is the excuse it provides to enjoy an Aperol or Campari spritz. We make them at home, too, and they bring back that warm Italian feeling.

Abstinence Spirits sells a range of non-alcoholic spirits products that are made in South Africa using the distilled essence of botanicals of the Cape Floral Kingdom. There are a variety of interesting NA spirits both bottled straight and used in NA RTD spritz beverages. We were tempted by the lemon spirits (I was thinking lemoncello), but could not pass up the Abstinence Blood Orange Aperitif, which is flavored with African wormwood, cinchona bark, allspice, clove, blood orange, and spice distillate.

We tried the spritz as directed with both tonic water and soda and the result was a split decision. I liked the tonic spritz because it reminded me of an Aperol spritz, and I’d definitely take a second glass if offered. Sue admitted the resemblance to Aperol but found the drink just too sweet (both the NA spirits and the tonic are sweetened). The soda spritz was less sweet but lacked a bit of the bitter punch we were expecting.

Two cheers, not three, for the Abstinence Blood Orange aperitif, but we will keep experimenting. Lots of innovation in the NA beverage category. Watch for our next report in a few weeks.

There is a lot of work to do to restore wine to the place (in the market, in society) that many of us believe it deserves. Here in America, for example, we have recently concluded the successful launch of

There is a lot of work to do to restore wine to the place (in the market, in society) that many of us believe it deserves. Here in America, for example, we have recently concluded the successful launch of  Come Over October and VITÆVINO are both relatively recent initiatives, but Wine in Moderation traces its history back to 2007-2008. Originally focused on Europe to provide a countervailing voice to neo-prohibitionist policies and rhetoric. It is now a global movement, although it has not caught fire here in America yet.

Come Over October and VITÆVINO are both relatively recent initiatives, but Wine in Moderation traces its history back to 2007-2008. Originally focused on Europe to provide a countervailing voice to neo-prohibitionist policies and rhetoric. It is now a global movement, although it has not caught fire here in America yet. A cynic, according to Oscar Wilde, knows the price of everything and the value of nothing. For some reason, this characterization is often associated with “dismal science” economists like me. Today’s Wine Economist column hopes to make an exception to Wilde’s rule by focusing on wine’s value problem and how understanding it can help explain recent market trends.

A cynic, according to Oscar Wilde, knows the price of everything and the value of nothing. For some reason, this characterization is often associated with “dismal science” economists like me. Today’s Wine Economist column hopes to make an exception to Wilde’s rule by focusing on wine’s value problem and how understanding it can help explain recent market trends. The global wine market is in flux these days and much of the attention is focused on falling consumption in the post-pandemic era. Global wine consumption actually peaked a few years ago, as the graph above shows, but the trend was disguised for a while by Covid pantry-stocking and other factors.

The global wine market is in flux these days and much of the attention is focused on falling consumption in the post-pandemic era. Global wine consumption actually peaked a few years ago, as the graph above shows, but the trend was disguised for a while by Covid pantry-stocking and other factors. The figure below provides a demand-side picture of the situation. Global white wine sales (by volume) held up better in the current climate than did red wine sales, so white’s share of the pie has grown. Changing production is a response to shifts in demand. Good news for white wine producers like New Zealand. Not-so-good for red wine producers like Argentina and Spain.

The figure below provides a demand-side picture of the situation. Global white wine sales (by volume) held up better in the current climate than did red wine sales, so white’s share of the pie has grown. Changing production is a response to shifts in demand. Good news for white wine producers like New Zealand. Not-so-good for red wine producers like Argentina and Spain. The changing color of wine shows up in both the data and on the store shelves. We have encountered more examples of white wines made from red grapes, for example, as producers look to align production with demand within the constraints of existing vineyard varieties. White Malbec from Argentina? It was the surprise hit of one of our tastings. White Pinot Noir from Oregon? Yes, that’s a thing now, too, and it can be very nice.

The changing color of wine shows up in both the data and on the store shelves. We have encountered more examples of white wines made from red grapes, for example, as producers look to align production with demand within the constraints of existing vineyard varieties. White Malbec from Argentina? It was the surprise hit of one of our tastings. White Pinot Noir from Oregon? Yes, that’s a thing now, too, and it can be very nice.

Is October 2024 the month you finally try non-alcoholic (NA) wine? Maybe you’ve never sampled NA wine before or perhaps you have and were disappointed. In either case, this might be a good time to see what’s going on.

Is October 2024 the month you finally try non-alcoholic (NA) wine? Maybe you’ve never sampled NA wine before or perhaps you have and were disappointed. In either case, this might be a good time to see what’s going on. October has sort of evolved into a month to think about how wine fits into your lifestyle. It started, I think, with the advent of something called Sober October, which is sort of an echo of Dry January. Why October? Because it rhymes with Sober, I suppose.

October has sort of evolved into a month to think about how wine fits into your lifestyle. It started, I think, with the advent of something called Sober October, which is sort of an echo of Dry January. Why October? Because it rhymes with Sober, I suppose.  You’ve probably seen the news from Europe. The headline on Politico read,

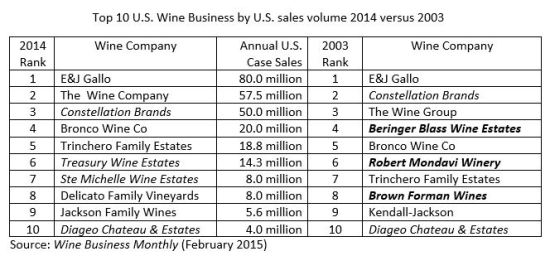

You’ve probably seen the news from Europe. The headline on Politico read,  We often talk about trends and problems in the wine industry, but I think we all know that wine isn’t a single business about which it is easy to generalize. Different countries or regions have different business characteristics, for example, and making and selling multi-million case brands like Gallo’s Barefoot differs greatly from much smaller and more local operations.

We often talk about trends and problems in the wine industry, but I think we all know that wine isn’t a single business about which it is easy to generalize. Different countries or regions have different business characteristics, for example, and making and selling multi-million case brands like Gallo’s Barefoot differs greatly from much smaller and more local operations. I recently discussed some of these wine economics themes and more with

I recently discussed some of these wine economics themes and more with  These are challenging times for many (but not all) consumers. Rising housing and interest costs are squeezing budgets. Pandemic-era stimulus check bank balances are going or gone. Student loan payments, paused for a time, are back again.

These are challenging times for many (but not all) consumers. Rising housing and interest costs are squeezing budgets. Pandemic-era stimulus check bank balances are going or gone. Student loan payments, paused for a time, are back again.

Collio DOC, which hugs the Slovenian border in north-east Italy, has long been known for its excellent wines and it is home to many strong private wine brands. Sue and I visited

Collio DOC, which hugs the Slovenian border in north-east Italy, has long been known for its excellent wines and it is home to many strong private wine brands. Sue and I visited  More recently there has been an effort to promote a trademark Collio wine bottle shape, which is also shown in the photo above. The distinctive bottle actually requires a special cork to seal it properly. Adopting it is a serious decision from a practical standpoint.

More recently there has been an effort to promote a trademark Collio wine bottle shape, which is also shown in the photo above. The distinctive bottle actually requires a special cork to seal it properly. Adopting it is a serious decision from a practical standpoint.